TypewrAIters

No LLMs were harmed in the making of this article

Firstly, we’d like to aknowledge there has been a most lengthy gap between our latest article and this. We have been busy with business development and other administrative tasks, with little time left for the substack. Now onto it:

As per usual we will allow the armchair twitter experts to comment on the trendy topic of the day, so no comments on the conflicts taking place in the middle east on this note (maybe next time regarding crude oil term structure and other energy/inflation related topics). We run a fund here and we comment only about our portfolio, market action and how our theses may or may not work.

We have been off to a decent start, we entered 2026 with a bold short position in financials, this has contributed almost half of our total return (up 8% ytd). We have taken profits on half the position and bought defensive sectors. On the duration side we are exposed to the 2 and 3 year tenors the most on a USD weighted view, but most of the duration exposure comes from the 10yr.

We consider the lack of a cut yesterday was (yet another) policy mistake by the Fed but given our current alpha we see no need to trade this just yet.

Short term rates are being repriced significantly today but we mantain a dovish view, we are partifularly impressed by the moves in SONIA today

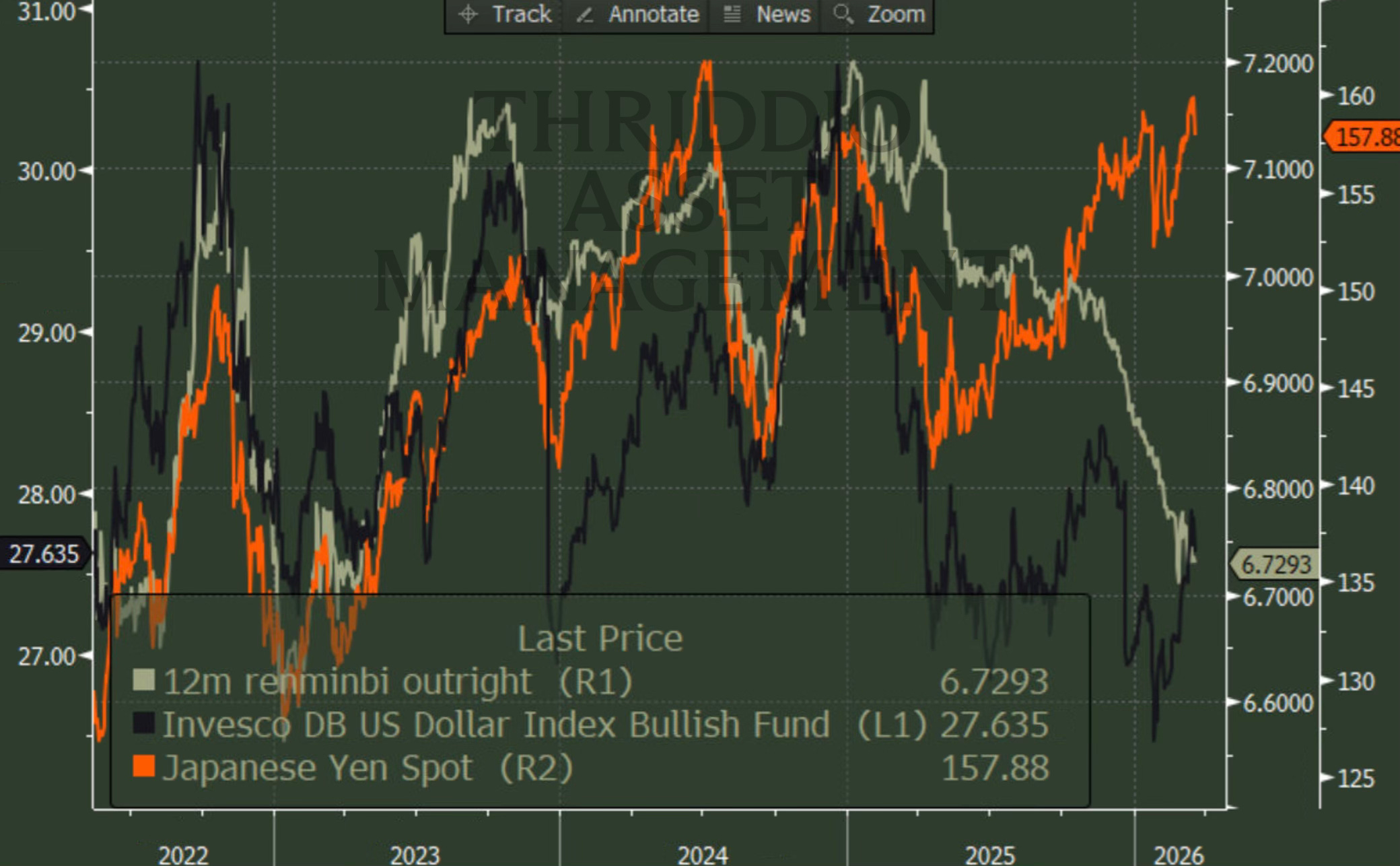

Along those lines there are a few other macro trends that have been surprising us, the break in correlation (or more adequately, cointegration?) between JPY, RMB and DXY. This happened back around November last year, and has been erratic. We are very intrigued by what is driving this disconnect.

Moving on to equities, we’d like to point out that if, AI is a bubble, then taking the dot com as reference, we’d still have at least one good strong rally left, buckle up!

Now whilst a lot of people swear by AI and many are sure this will replace most office jobs, we are in the camp that believes these tools are more like super enhanced typewriters, for sure, back when typerwiters were introduced they transformed the workspace and replaced scribes, clerks, etc. It obviously had significant changes in society, productivity and the way we communicated, a huge change indeed, but not the end of work, nor a collapse in the workforce. But maybe we are too optimistic/naive? In any case we have a structural software underweight but given the chart above we could consider a tactical long.

Briefly commenting on credit markets, while private credit headlines seem concerning, public credit has shrugged it off, no stress visible in public spreads and none to be found by looking at SOFR implied vols, nor FF open interest, effective fed funds vs GC, or any other stress indicators. Sure JPM tightened conditions to those private credit funds and some investors are trapped in “semi”-liquid vehicles, but the only places where one can see these concerns are BDCs and the publicly traded equities of the general partners. We wouldn’t like to be a GP staker at the minute.

Looking forward we remain overweight energy, we will probably cover the remaining short in financials as it continues to break down, and we are keeping our eyes on the relative US vs RoW chart, if it has peaked, then the trend reversal could last years and this would have huge ramifications for asset allocators who are overweight US assets (most of them, including us) and would prompt us to reevaluate the structural asset allocation.

This is for informational purposes only, it should not be considered as investment advice and does not constitute any offer or solicitation to subscribe or redeem. Investment involves risk. Please consult a licensed investment professional before taking investment decisions.

All charts and graphs copyright © Bloomberg Finance L.P.

P.S., something that caught our eye regarding the near east: