Inflection point?

Not a tariff commentary

Despite a rather wrongly timed call shorting gold miners, March was a great month for our portfolio, up 55bps in absolute terms while the global macro peer group was down -2.45% .

Top contributors were of course our hedges (short SPX, tech and semiconductors) followed by UL 0.00%↑, MOS 0.00%↑ and our long end treasuries.

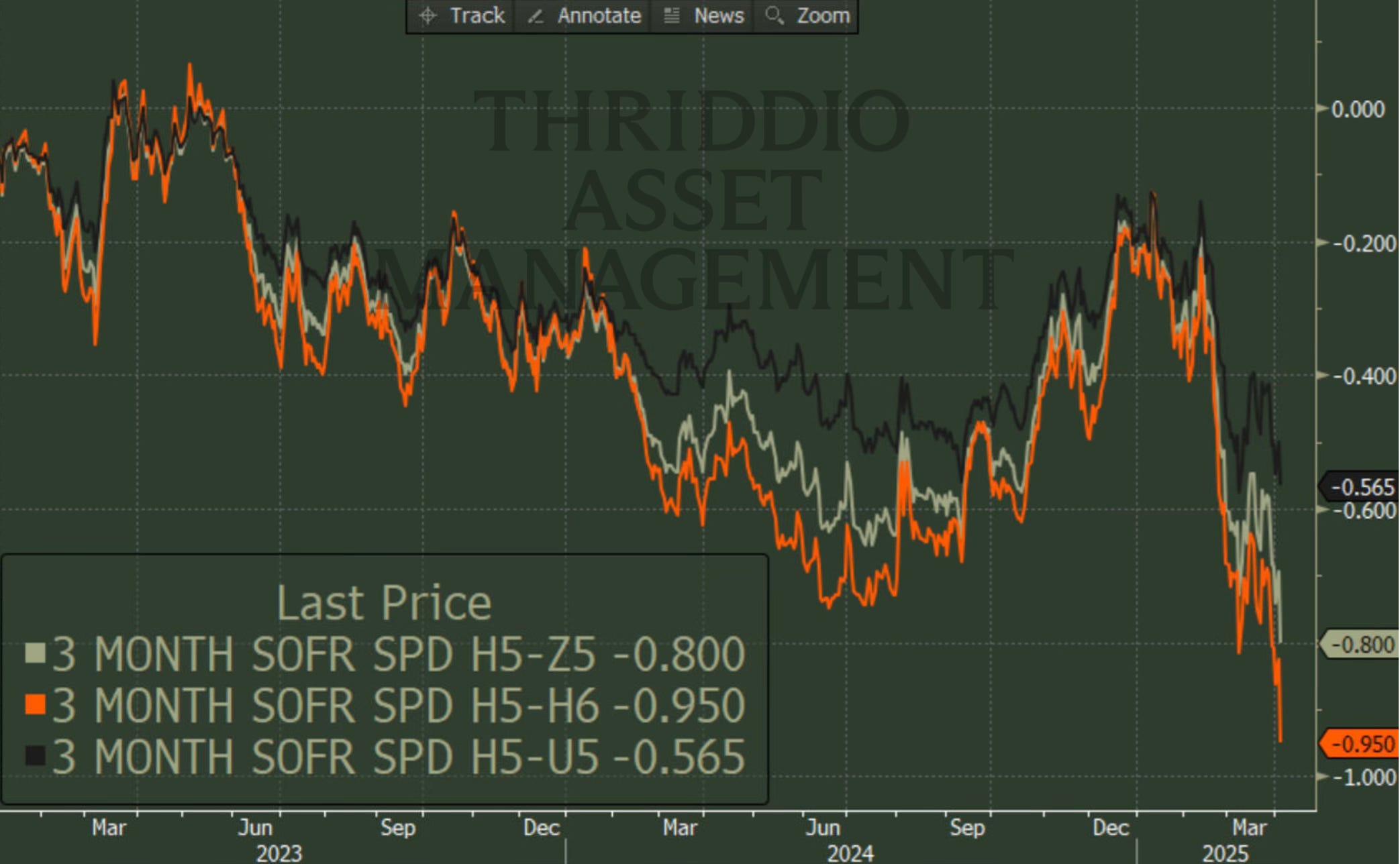

Commenting on the latest money market moves, we are thrilled to see our views on lower rates coming back to the table with the March2025-March20206 spread making new lows and over 3 cuts priced in from now on to year end.

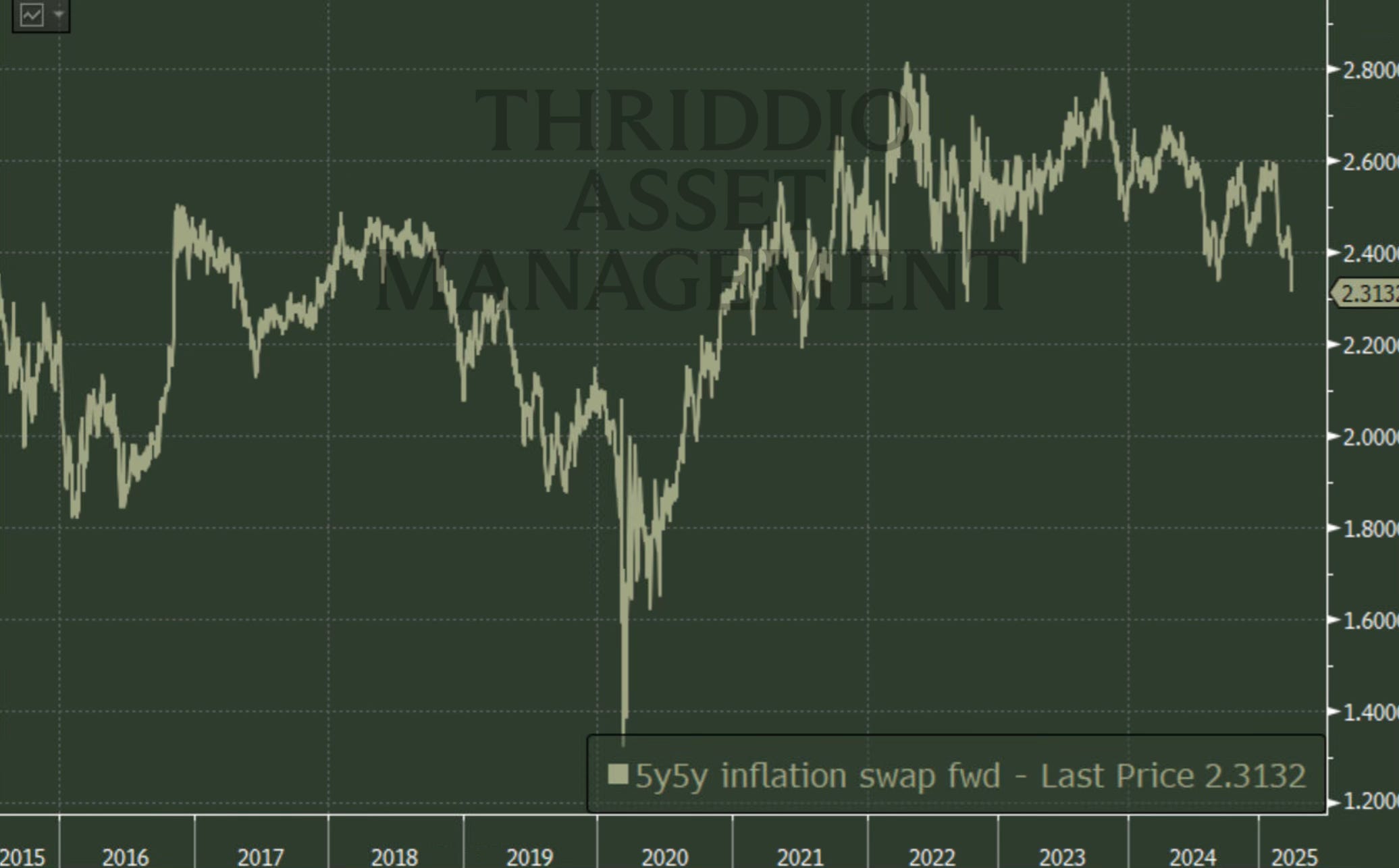

This is unsurprising given where the 5y5y inflation swap has been all year and now at 3 year lows. And while the shorter ones have moved higher (2yr breakevens are at 2023 highs now) longer trends seem to be to the downside.

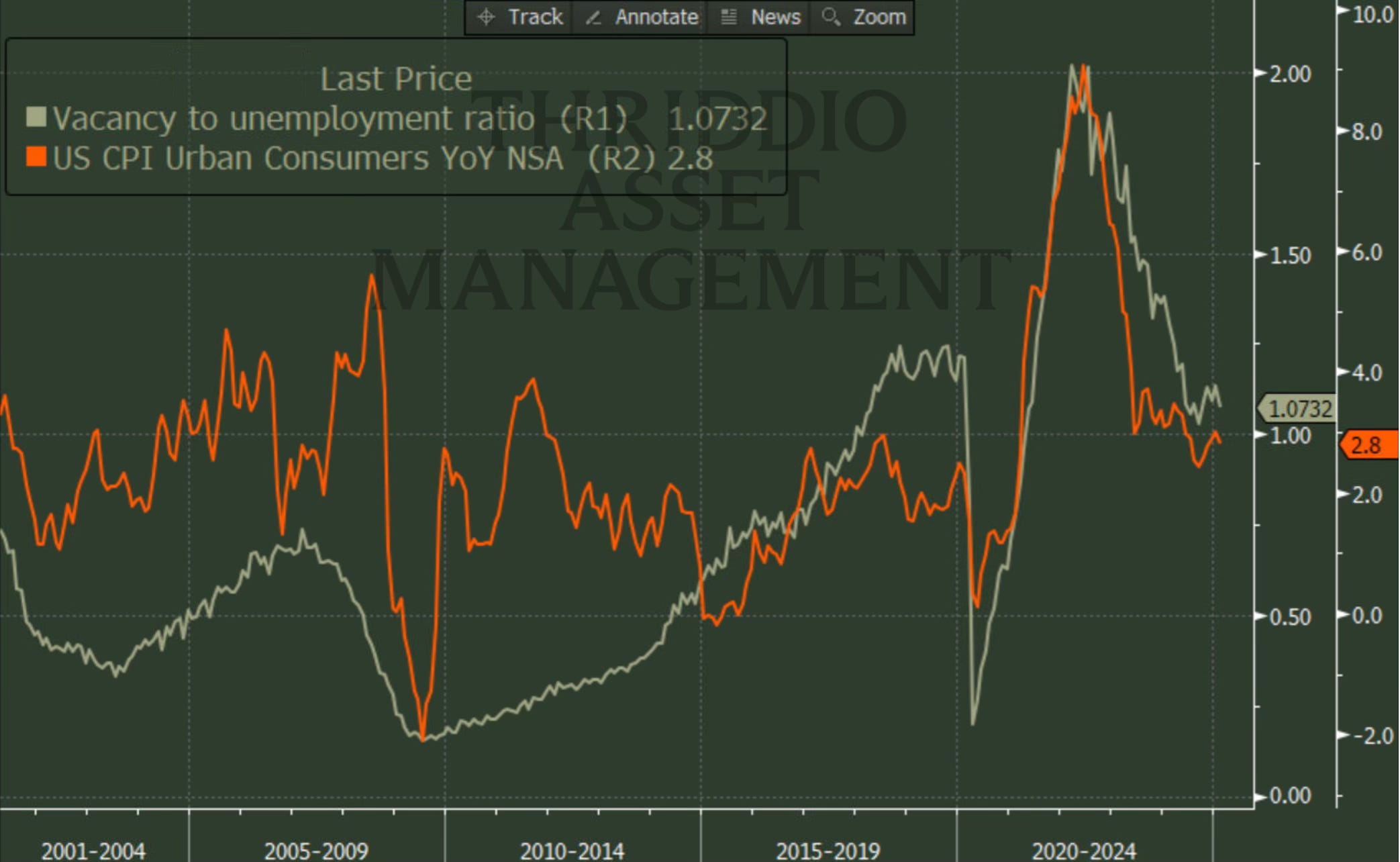

On the macro aspect we would like to point out that the vacancy to unemployment ratio has been steady for the last months and this is also a driver of inflation, it seems to us like this will continue to move downwards which would be an ease on inflationary pressures as seen in the chart below (not the most statistically robust, but this is not an academic writing) :

Moving on to equities, while crack spreads have bounced nicely, this has not translated into any outperformance for our XOP-XLE and KSA 0.00%↑ holdings . We hold these positions as our structural view has not changed and we have risk budget to tolerate the associated volatility.

Another interesting development YTD is the current dispersion in broad equity markets with european markets up about 12% in USD terms while US markets are down 8%, rest of the world is broadly up resulting in the All Country World index down just over 300 bps.

Avoiding the rather overpriced sectors has been a good trade for the time being, and while the relative outperformance of nasdaq vs sp500 topped out back in july, we cannot help but to wonder if this will be a change in the long term trend or just a repeat of 2022 when tech and growth sectors suffered massively only to bounce nonstop the following year.

Lastly, while the most recent market action has been rather volatile, our portfolio is very well positioned for this kind of environment, we expect a quick bounce in the coming days but volatility to remain high. We are up 800 bps vs benchmark YTD, we estimate this places us in percentile 99 of the peer group. The portfolio remains unchanged as we feel most comfortable with current risk profile.

This is for informational purposes only, it should not be considered as investment advice and does not constitute any offer or solicitation to subscribe or redeem. Investment involves risk. Please consult a licensed investment professional before taking investment decisions.

All charts and graphs copyright © Bloomberg Finance L.P.