Disinflating the burden

Something has to give

As frequent readers will know, we have not been expecting any inflation for a while. Our portfolio benefited greatly from some reflationary trades back in 2021-22 but that was about it. We keep a close eye on many inflation indicators, commodities, surveys, etc. and overall we have not been able to call for inflation. And yet, the latest print in Citi’s Inflation Surprise index surprised us by printing its lowest reading in almost a decade. We were definitely not expecting such dovish reading

If, indeed, inflation keeps trending lower, we would expect nominal yields to follow, otherwise at these postive real rates it would be difficult for the US to roll the 4.5 trillion in debt that mature over the next 18 months. This is linked with the budget deficit story; in our view in order for the US to narrow the deficit, real rates would need to go higher, but then how can the debt be financed? Something has to give

Following with this philosophical discussion we wonder if we will we see a return of negative yields over the next 2 years?

Enough of philosophical discussion and onto more practical things. Since our last note we have done a couple of changes to the portfolio, we bought some RIOT 0.00%↑ as a quick proxy to the crypto trade, our current target price for that one is 11 given that most of the market looks a bit tired and quite a few names look like a double top or just sideways which is not bullish for the overall risk on environment that has prevailed the last 5 weeks. We also added some long bonds, we are underwater on that trade.

Continuing with our favourite metal, gold, we have decided to unwind some of our structural long position, we may regret it if it breaks out again but the movement has been too quick, and while it is always a core part of our portfolio. We are targeting the 2800 handle to buy this portion again, otherwise we are okay buying back higher. We have held this since inception at around $1700. A haircut is not unreasonable.

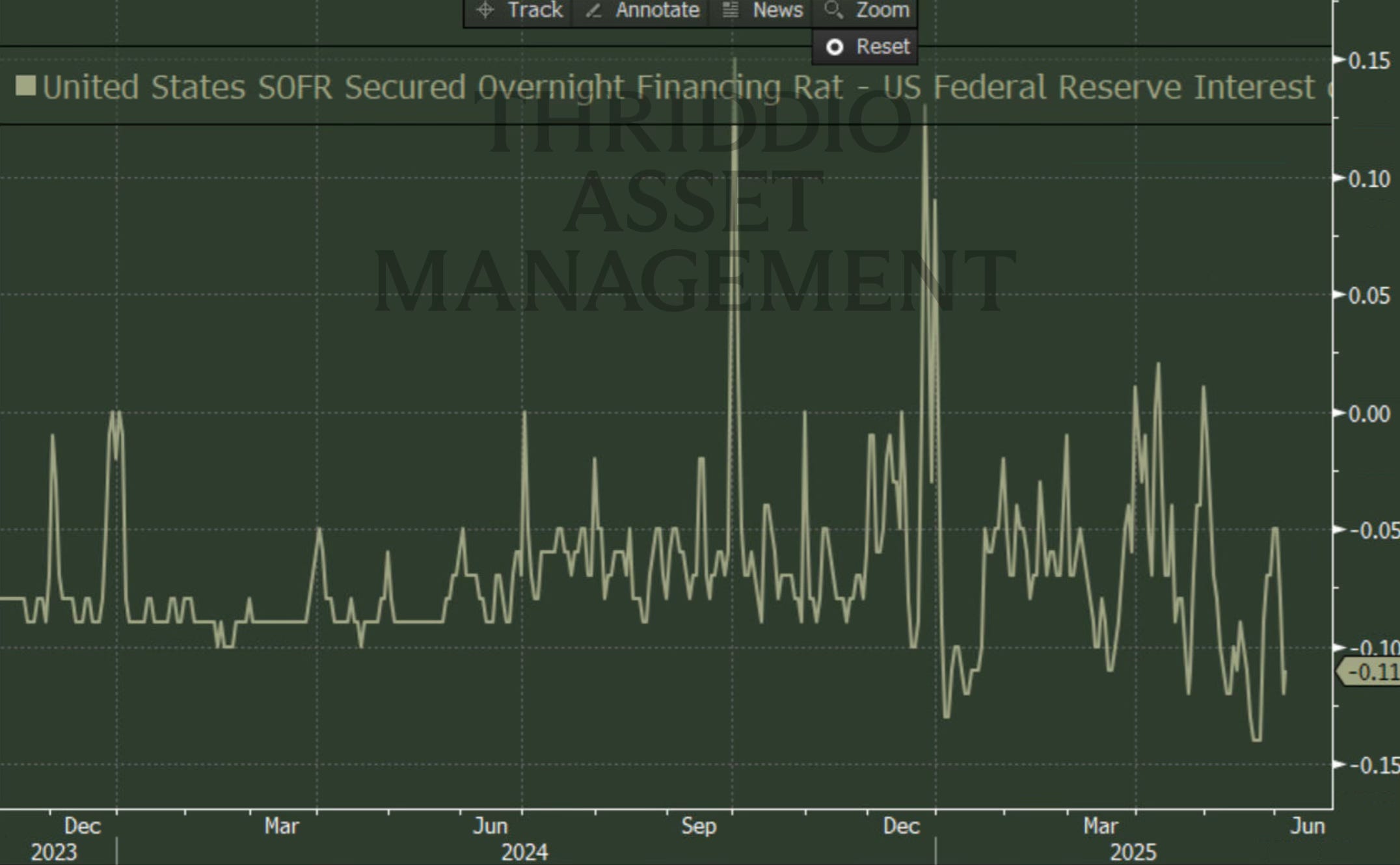

All things seem relaxed in money markets with both SOFR volatility easing and overnight rate trading below interest on excess reserves. (Stress in money markets would be overnight rate trading higher than IOER) So no news there.

Lastly while we are also structural bulls on the uranium trade, the current resistance level seems strong and whilst the market pierced through it last week, we would like to see it holding up here for at least a couple of weeks before calling it a breakout, a lot of single names seem like they are in a double top, today’s breakout is mostly due to $CCJ, gap up, lets wait for that gap to be filled and see how the broader sector behaves.

This is for informational purposes only, it should not be considered as investment advice and does not constitute any offer or solicitation to subscribe or redeem. Investment involves risk. Please consult a licensed investment professional before taking investment decisions.

All charts and graphs copyright © Bloomberg Finance L.P.

Good stuff man. Hope you’re well 👌🏻